Most small business owners have no idea how much they’re overpaying on credit card processing. You see a rate on the website — 2.6%, maybe 2.9% — and you sign up. But when the statement arrives, the math doesn’t add up. Where did the extra 0.7% go? Why does this transaction charge more than that one? Why are there five different fees I’ve never heard of?

The answer lies in how credit card processors price their services. And understanding the difference between interchange-plus pricing and flat‑rate pricing could save you thousands per year.

The Three Pricing Models Explained

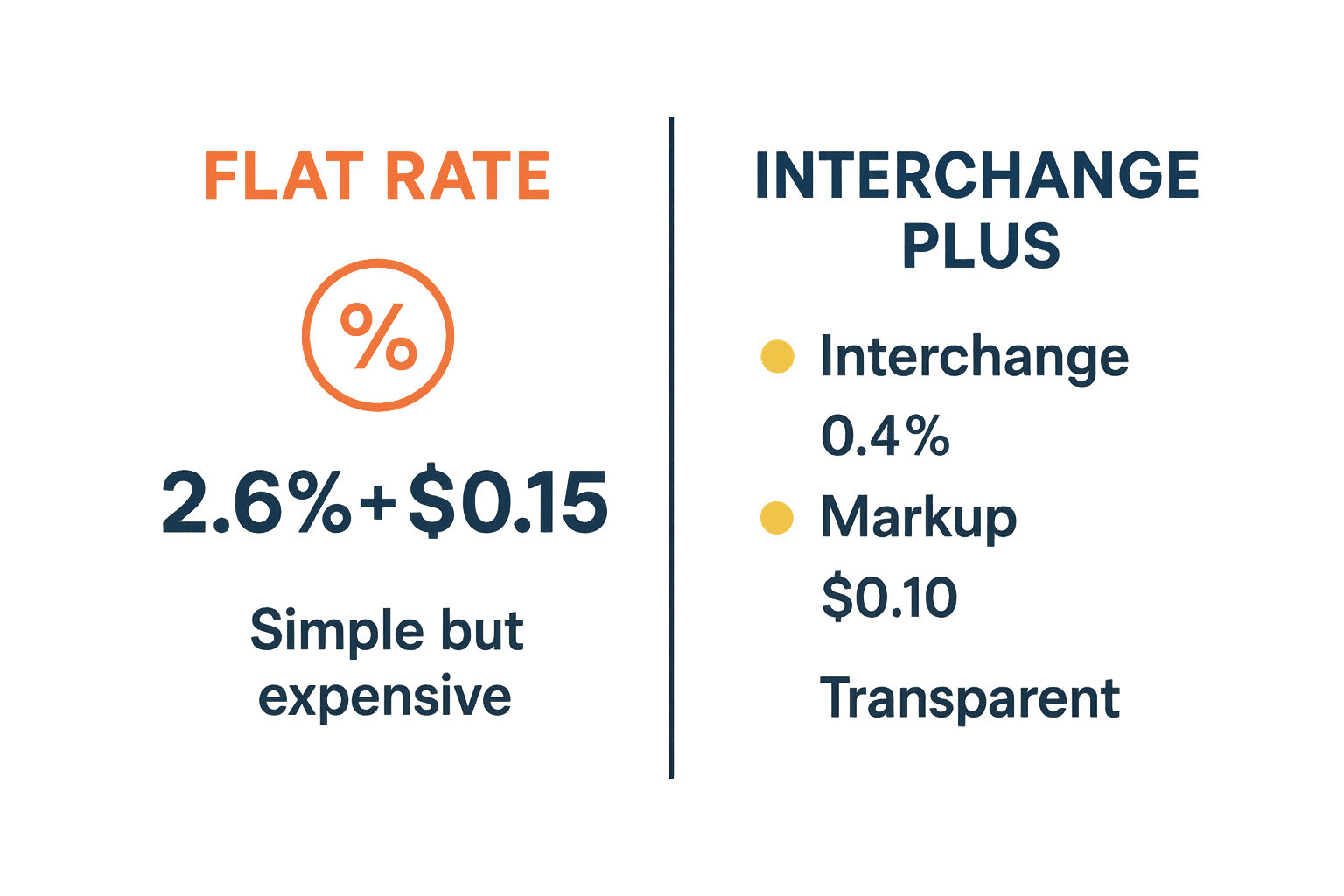

Flat-Rate Pricing (Square, PayPal, Stripe)

Flat-rate processors charge a single percentage plus a small transaction fee for every payment, no matter what card your customer uses or how they pay.

| Processor | In-Person Rate | Online Rate | Monthly Fee |

|---|---|---|---|

| Square (Free) | 2.6% + $0.15 | 3.3% + $0.30 | $0 |

| Square (Plus) | 2.5% + $0.15 | 2.9% + $0.30 | $49 |

| Square (Premium) | 2.4% + $0.15 | 2.9% + $0.30 | $149 |

| PayPal | 2.99% + $0.49 | 2.99% + $0.49 | $0 |

| Stripe | 2.7% + $0.05 | 2.9% + $0.30 | $0 |

The promise: Simple, predictable pricing. You know exactly what you’ll pay per transaction.

⚠️ The Reality

That “simple” flat rate includes a hidden markup. The processor pays the card network an interchange fee (let’s say 2.3% + $0.10), charges you 2.6% + $0.15, and keeps the difference without telling you. This is called the interchange spread.

Interchange-Plus Pricing (AGMS, traditional merchant accounts)

Interchange-plus pricing breaks every fee into separate line items on your statement:

- Interchange fee — Set by Visa/Mastercard, passed through at cost

- Assessment fee — Card network fee (typically 0.11–0.15%)

- Processor markup — Your agreed‑upon fee (typically 0.3–0.8%)

💡 Example Transaction

Customer swipes a Visa debit card for $100:

- Interchange fee: 1.80% + $0.10 (what Visa charges)

- Assessment fee: 0.11% (what the card network charges)

- Processor markup: 0.50% + $0.10 (AGMS fee)

- Your total cost: 2.41% + $0.20 = $2.61

Every fee is visible on your statement. No surprises. No hidden spreads.

Tiered Pricing (Bundled/Qualified Rates) — Avoid This

There’s a third model you should know about — and mostly avoid. Tiered pricing bundles transactions into “qualified,” “mid-qualified,” and “non-qualified” buckets, each with a different rate.

🚫 Why Tiered Pricing Is the Worst of Both Worlds

The processor decides which tier each transaction falls into, often placing most in the expensive “non-qualified” category. What looks like a 1.5% rate in marketing materials often becomes 3.5%+ on your actual statement. No transparency. No auditability. No negotiation leverage.

If you’re on tiered pricing, get a statement analysis immediately. You’re almost certainly overpaying.

Subscription Models (Stax, Payment Depot)

A newer hybrid: pay a monthly subscription fee ($49–$99/month) for access to interchange-only pricing with zero or minimal markup per transaction.

Best for: High-volume merchants ($30,000+/month) where the flat subscription is cheaper than percentage markups. A business processing $50,000/month might pay $99 + interchange instead of 0.5% markup on $50,000 ($250).

Trade-off: If your volume drops, you’re still paying the subscription. Less flexibility than pure interchange-plus.

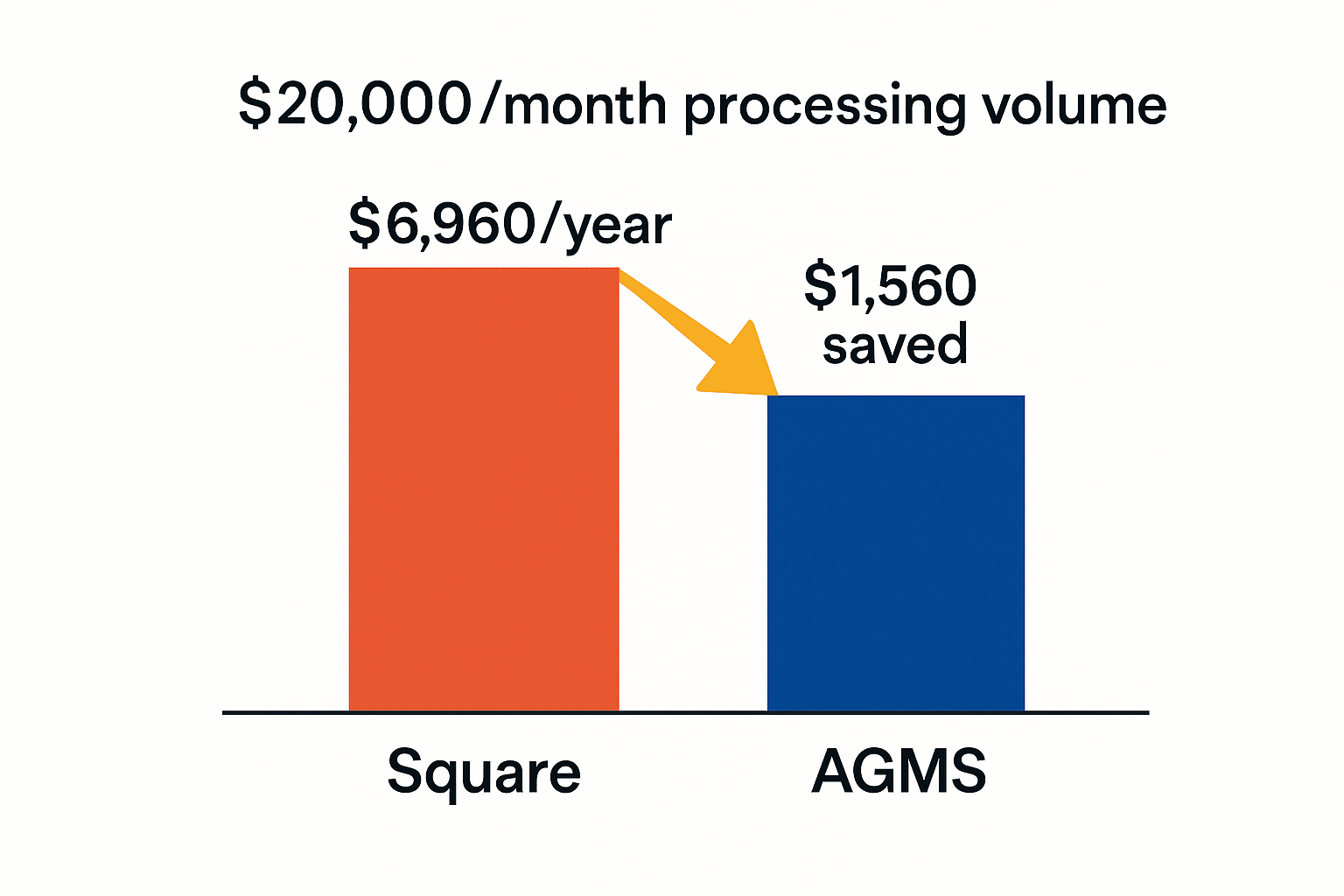

Why the Difference Matters: Real Math

The math on $20,000/month in card sales

Scenario: You process $20,000 per month with mixed transaction types (60% card-present, 40% card-not-present)

| Square (Flat Rate) | AGMS (Interchange-Plus) | |

|---|---|---|

| In-person (60%) | $12,000 × 2.6% + $0.15 = $315 | Lower interchange on swipe/tap |

| Online (40%) | $8,000 × 3.3% + $0.30 = $267 | Transparent, slightly higher |

| Monthly Total | $582 | ~$450 |

| Annual Total | $6,984 | ~$5,400 |

$1,560 – $2,400

per year on $20,000/month volume — and that’s conservative

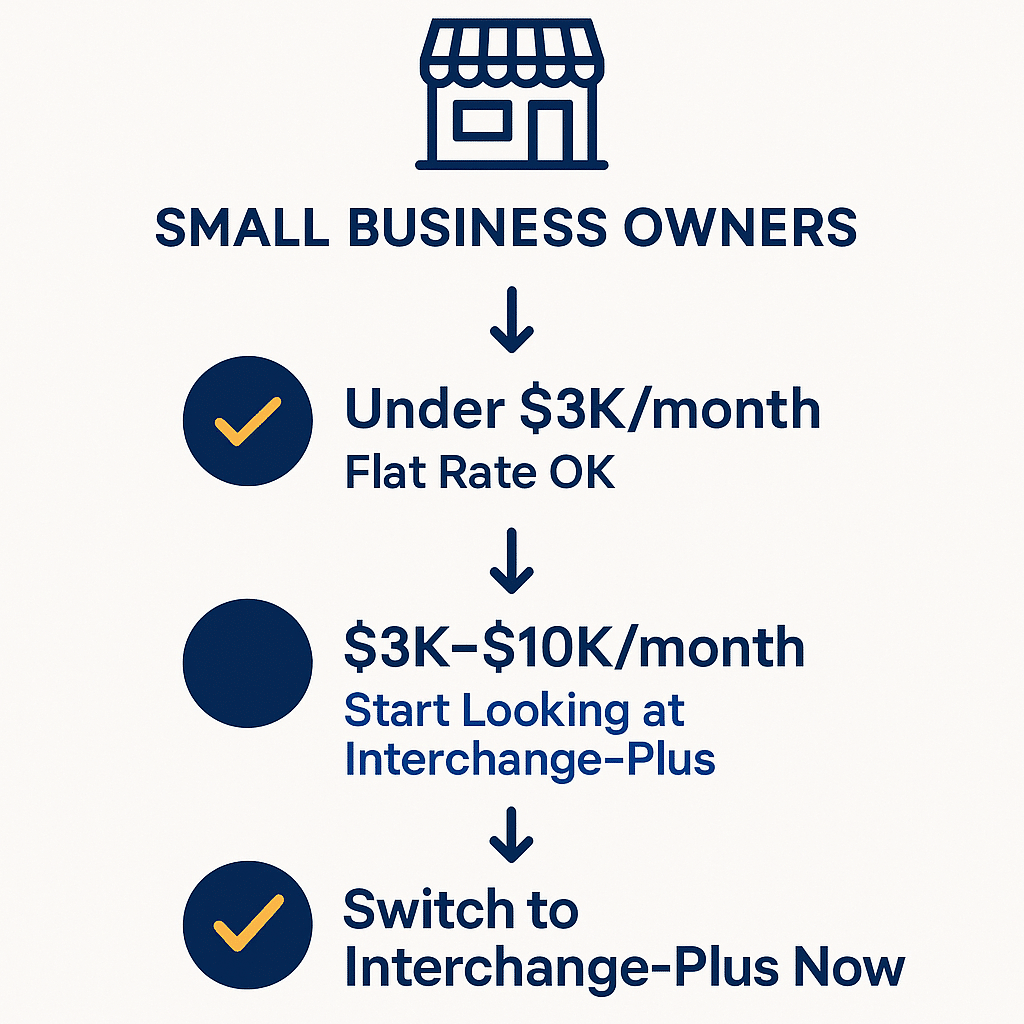

When flat rate actually wins

Flat-rate pricing isn’t always bad. It makes sense if:

- You’re very small: Under $3,000/month, the math is close enough that simplicity wins

- You have a mix of expensive and cheap cards: Flat-rate “averages” everything, so you don’t pay extra for premium rewards cards

- You truly cannot manage statements: If you genuinely cannot read a PDF statement, flat rate removes that cognitive load

But once you cross $5,000/month, interchange-plus usually pays for itself. And if you’re in a high-volume vertical (restaurants, retail, e-commerce), the savings accelerate fast.

The Hidden Problem with Flat Rate

1. No transparency = no control

With flat-rate pricing, you can’t see what you’re actually paying the card networks. You might be overpaying because:

- Your processor got a volume discount they didn’t share

- You qualified for a lower tier but never got downgraded

- You’re on a promotional rate that expired

💡 The Interchange-Plus Advantage

With interchange-plus, you can audit your own fees and negotiate: “I see I’m paying 0.7% markup. Industry standard is 0.4%. Let’s adjust.” Try doing that with Square.

2. Rate hikes come without warning

Square raised rates by 14% in January 2026 without telling merchants beforehand. You just started paying 3.3% instead of 2.9%. We covered the full impact in our Square Price Increase 2026 guide. With interchange-plus, your markup is written into your contract and cannot change without your signature.

3. The “free” plan costs more than you think

Square’s “no monthly fee” pitch sounds great until you realize you’re paying $300/month in processing fees instead of $150. That’s $1,800/year in hidden markup — enough for new equipment, a part-time employee, or marketing. You’re already subsidizing their platform — why not pay for transparency instead?

4. Hidden 2026 rate increases you won’t see on flat-rate statements

📢 April 2026 Update: Visa & Mastercard Rate Changes

Visa killed the Level 2 program — effective April 18, 2026, businesses can no longer qualify for discounted B2B rates using basic tax and zip code data. Business card rates increased by 65-75 basis points for merchants not meeting the new CEDP standards.

Mastercard introduced Small Ticket rates in Q2 2026 — transactions under $5 now have specialized interchange rates. Coffee shops, food trucks, and vending operators should see lower costs — but only if they’re on interchange-plus. Flat-rate merchants won’t see the savings.

If you’re on flat-rate pricing, these changes are invisible to you. The processor absorbs the cost — then passes it along in your next rate hike.

Who Pays Most Under Flat-Rate Pricing?

High-volume merchants

If you process $50,000+/month, the spread adds up fast. A 0.5% difference on $50,000 is $250/month, or $3,000/year. That’s one part-time employee.

Businesses with many rewards cards

Premium travel cards, corporate cards, and debit cards with cash-back rewards carry the highest interchange fees. Flat-rate processors “average” this by charging everyone the highest rate. If most of your customers use basic Visa/Mastercards, you’re overpaying.

International businesses

Foreign transaction fees under flat-rate processors are hidden in the spread. With interchange-plus, you see exactly what you’re charged for international cards and can shop competitive FX rates. If fund holds are a concern, read our guide on how to avoid payment processor freezes.

Restaurants and food trucks

Tips affect interchange calculations. Under flat rate, you pay the spread on tips too. With interchange-plus, you only pay actual costs plus your markup.

The AGMS Difference

Interchange-plus with human support

Most interchange-plus processors are “low-touch” — you get your terminal, your rate, and a phone number that sometimes rings. At AGMS, you get:

- A dedicated account manager — Someone who knows your business, at 866-951-2467

- Next-day funding — Your money, when you need it

- No fund freezes — Your own merchant ID means no risk of algorithmic account shutdowns

- Hardware flexibility — Choose from PAX A80, SwipeSimple, Clover, or Quantic POS

- Zero-processing option — Cash discount program at $30/month flat

Example: Restaurant owner switching from Square

| Before (Square) | After (AGMS) | |

|---|---|---|

| Volume | $35,000/month | $35,000/month |

| In-person fees | $21,000 × 2.6% = $546 | $35,000 × 2.4% = $840 |

| Online/phone fees | $14,000 × 3.3% = $462 | |

| Monthly Total | $1,008 | $840 |

| Annual Total | $12,096 | $10,080 |

| Annual Savings | $2,016/year |

…and this restaurant now has a dedicated account manager who actually picks up the phone.

Common Objections (Addressed)

“But interchange-plus is complicated”

It’s not complicated — you’re just not used to seeing the breakdown. Here’s what your statement shows:

- Interchange: What Visa/Mastercard charges (fixed by the networks, we can’t change it)

- Assessment: Small network fee (~0.11%)

- Markup: Our fee (negotiable, locked in your contract)

That’s it. Once you see it a month or two, it makes more sense than the flat-rate mystery fee.

“I already have a great rate with Square”

If your rate really is 2.6% in-person, you’re probably on the “free” plan. Consider: Square’s Premium plan charges 2.9% online with a $149/month subscription. At what volume do you break even? About $50,000/month in card sales. If you’re over that, you’re leaving money on the table.

“I don’t want to deal with switching processors”

Most merchants can be live with AGMS in 2–3 weeks. We handle merchant account setup (24–48 hours), terminal programming, test transactions, and team training. You can run both processors during the transition — zero downtime.

Which Model Is Right for You?

Flat rate is fine. The math works out close enough that simplicity wins.

Start looking. Interchange-plus probably saves you money soon.

You should already be on interchange-plus. If you’re not, you’re leaving thousands on the table.

Ready to Stop Overpaying?

AGMS offers free rate comparisons — we’ll analyze your last 3 months of statements and show you exactly what you’d save with interchange-plus pricing. No commitment, no obligation.

Get Your Free Comparison

Call 866-951-2467

A real human will answer. New merchant account set up in under 2 weeks.

Frequently Asked Questions

What is the typical interchange-plus markup?

Most processors charge 0.25–0.80% + $0.10–$0.20 per transaction. AGMS typically prices at 0.3–0.6% + $0.10–$0.15, depending on your volume and industry.

Can I switch from flat rate to interchange-plus mid-month?

Yes. Most processors allow you to terminate at any time, though you should check your contract. At AGMS, we can have you running in parallel with your old processor for a week or two so there’s no disruption.

What if your interchange-plus costs more than my flat rate?

This is rare, but it can happen with very low-volume merchants using mostly premium rewards cards. If you switch and the math doesn’t work out, we’ll adjust your markup or move you to a flat-rate plan — no penalty.

Are there hidden fees with interchange-plus?

The whole point is there are no hidden fees. If you see a fee you don’t recognize, call your account manager and ask. If we charge it, we should be able to explain it in one sentence.

Does interchange-plus work with mobile readers and Tap to Pay?

Absolutely. AGMS supports all hardware types: PAX A80, SwipeSimple Bluetooth readers, Apple Tap to Pay on iPhone (via AGMSPay app), and full POS systems like Clover and Quantic. See our full credit card terminal lineup.

What about chargebacks and refunds?

Chargeback fees are typically $15–$30 per dispute. With interchange-plus, you see this as a line item. With flat rate, it’s buried in your processing statement. To minimize disputes, use AVS, CVV verification, and 3D Secure for online payments.

Do all processors use interchange-plus?

No. Most aggregators (Square, PayPal, Stripe) use flat rate. Traditional merchant account providers (AGMS, first-party ISOs) use interchange-plus. Some “hybrid” processors use a modified interchange-plus that still includes hidden margins on certain card types.